When the Talking Stops

Fewer words, louder reactions, and a market with no trajectory.

Inside: What happens when the Fed decides to say less, why dual-class founders pay a price for silencing their shareholders, and what a tipped firework on the Fourth of July says about this market.

A Very Small Surface Area

One of the most scrutinized communicators in the world just decided to say less.

The new Fed chair has decided to dismantle the communications system his predecessors spent decades building. Forward guidance is out. No more explaining how data becomes decisions. The post-meeting statement was just cut in half, and press conferences are officially under formal review. At his first one, he declined to answer question after question on the grounds that doing so would amount to giving guidance. He’ll still take the questions. He just won’t answer them.

The rationale is signal purity. The idea is that if markets stop parsing everything through what the Fed might do next, the Fed can see the economy more clearly and act more independently. But my read is that he believes markets have been coddled. That fifteen years of dot plots and tightly choreographed pressers have taught investors that the Fed will always telegraph its next punch. And he wants that to end.

I understand the impulse. I really do. In some respects, I agree with the premise. But I think the experiment will ultimately deliver the opposite of what he wants.

Companies face this exact same choice. How much do you show the market?

Look across any earnings season, and you’ll see the full spectrum on display. Some CEOs are now using AI avatars to read their prepared remarks and avoid subconscious tells. Some companies have stopped holding calls altogether or stopped taking live questions. Most still run earnings calls so tightly scripted that they are stripped of all humanity, too clinical and boring for literally anyone to actually want to listen. And then there’s the other end. Marc Benioff runs Salesforce’s earnings like a live television production. Producers are cutting from camera one to camera two. His whole team is on set. Analysts on screen, asking their questions live. It’s the best earnings call I’ve ever seen, and not because of the craftsmanship. Because it’s human, interactive, and everyone on it, analysts included, clearly wants to be there.

Every one of those formats is an answer to the same question the Fed just answered. How much surface area do you want to give the market?

Here’s the argument I’ve made to clients for years: conversation is how discovery happens. For a public company, price discovery, obviously. But also the discovery of you. How you think, what you do under pressure, whether your words and your actions rhyme. When you’re in constant conversation with the market, that discovery runs continuously, in small increments. Nobody ever learns too much at once.

But scarce conversation doesn’t stop the discovery. It defers it. The questions pile up, the estimates drift for months in different directions, and everything the market would have learned about you gradually now has to be learned all at once — against a few sentences when you finally break your silence.

That’s a lot of activity across a very small surface area.

And notice that surface area isn’t word count. An avatar reading a script is technically “speaking” and producing a lot of words in the process. A tightly scripted, clinical earnings call is technically a call. But there’s no life there and nothing real for the listener to parse. In other words, a company can “talk” endlessly and still give the market almost no human surface area at all.

This is the part the new Fed chair misses. Speak rarely, and you won’t get calmer markets. You’ll get markets that build pressure between statements and release it all at once when there’s finally something to decode. The old regime’s endless communication wasn’t coddling. It was load-spreading. A hundred small statements, each absorbing a little interpretation, so that no single one had to absorb it all. Estimates got corrected while the corrections were still cheap. Bad news arrived in pieces.

Now, I’ll admit the old regime wasn’t exactly freewheeling either. Powell was heavily scripted, and to some extent, that runs counter to my argument. But look at the volume. The chair stood for live questions after every decision. Scripted as he had to be, given that his words steer global markets, Powell was out there. You can be careful with every sentence and still be constantly in conversation. What you can’t do is disappear entirely and call it discipline.

And his decisions are already having an impact in ways he perhaps also didn’t predict. The governors and regional presidents haven’t gone quiet, and as a result, analysts are now placing even more attention on them, not less. Think about that. He shrank his communications surface area, and the market immediately went looking for a replacement. The scrutiny didn’t stop. It re-routed to whoever is still talking.

Here’s where this stops being a story about the Fed, or even about public companies, frankly, because this is how being understood works everywhere in life.

Think about a boss who surfaces twice a year at an all-hands meeting. Every sentence gets parsed endlessly because it’s all anyone has to go on. Think about the manager who goes silent for three weeks and then schedules a meeting — nobody assumes it’s good news, because silence never reads as neutral. It reads as looming. Think about waiting for a call from your doctor. The longer the wait, the more your imagination fills the empty space, and the more the eventual words have to carry.

Some communicators believe that speaking less makes each word more powerful and lean into that persona. And it does. But not always in the way they hope. It makes each word more volatile. Power without control.

Full disclosure: I am not the quiet type. Ask anyone who’s worked with me — or better yet, ask my wife — and they’ll tell you I don’t always stop talking when I should. As I’ve told her for nearly three decades, I am keenly aware of my flaws. And someday I might even get around to working on them! But that’s me. For better or worse.

And it’s probably why I trust this idea. Discipline is not about quantity. It’s about what you claim. I show up often, speak freely, and I’m careful with my promises. That combination is what keeps any single statement from having to carry the entire load.

The F-Word

There’s an F-word that tends to get people a little uncomfortable in boardrooms.

Not that one.

Though I’ll quickly confess to a rule from my early consulting days. In the first meeting with a potential client, I dropped the real f-bomb. Only once. Always on purpose. I wanted you to know exactly who you were hiring, right from the start, so there were no surprises later. And in all those years, no one even flinched. In fact, the room usually relaxed. As I look back, it turns out I wasn’t just telling them who I was. I was giving everyone permission to be themselves.

Hold that thought.

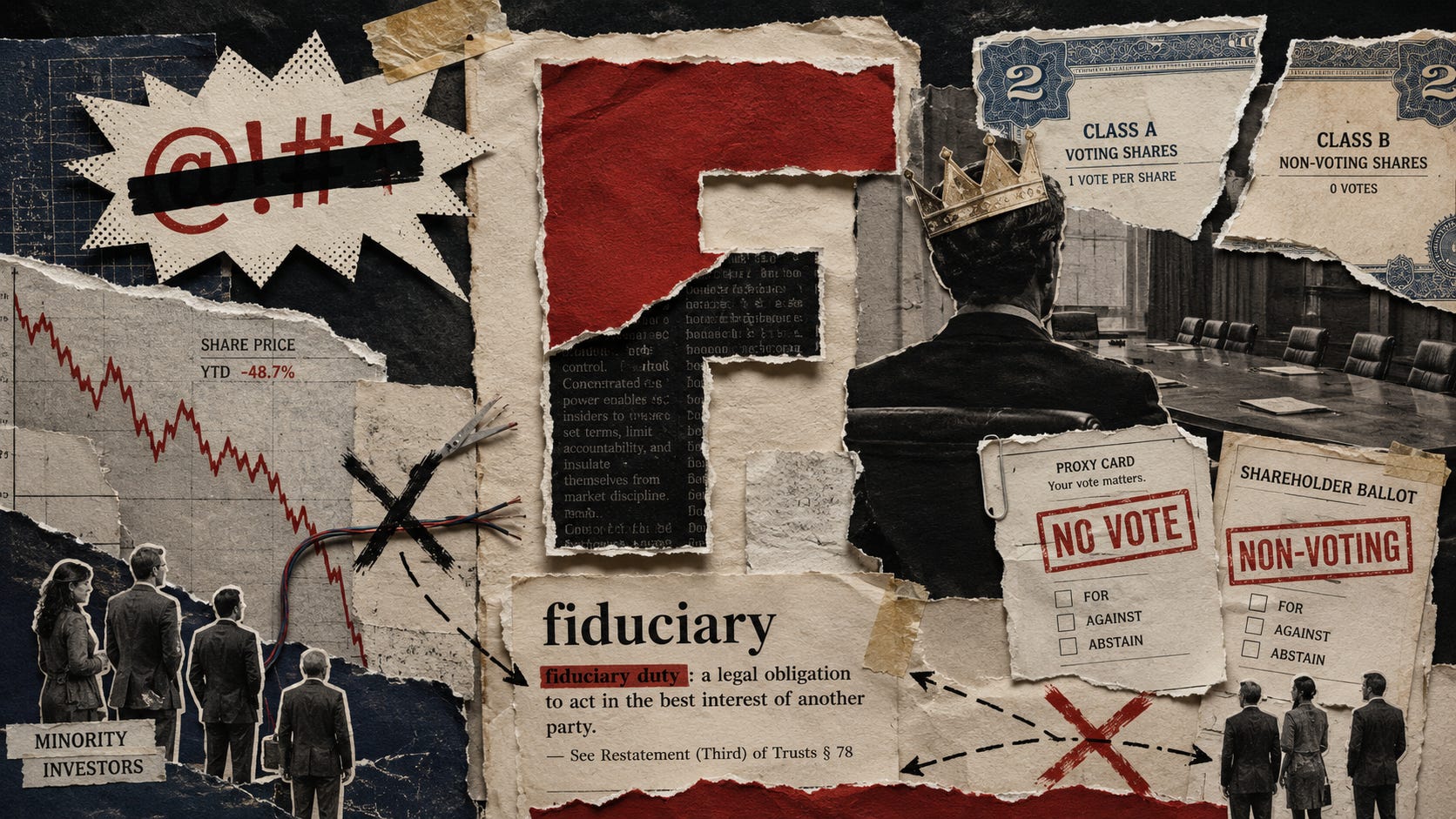

The F-word I actually mean is this one: Fiduciary.

It might be the most powerful word in business. And it sometimes feels like it’s quietly becoming the most avoided. Nowhere is that clearer than in the structure that has become the default for far too many companies. The dual-class share.

In the nineties, fewer than 10% of tech companies went public with multiple share classes. Last year, it was over 40%. Scan the recent large IPOs, and the structure is clearly no longer the exception; it’s become a standard. Founders get all the votes, and public shareholders bear the risk.

To be clear, dual-class shares don’t automatically destroy value. Alphabet has run this way for two decades and compounded magnificently. Though they’ve arguably come a long way from the original “don't be evil” motto. But the structure didn’t produce the outcome. It just guaranteed nobody could interfere with it. That’s the real point. A dual-class structure isn’t a verdict on a company. It’s leverage on the judgment of a small group of deciders. In my world of investor relations, it severs the feedback loop. Shareholders can still talk. They just can’t be heard. By that I mean a vote that cannot change an outcome isn’t a voice. It’s noise. In Alphabet’s case, when the judgment at the top has been right, you never notice the brakes are missing.

And then there’s Snap.

Three classes of stock. The Class A shares that actually trade carry zero votes. The two co-founders control roughly 95% of the voting power between them, and they’ve signed a proxy agreement to vote each other’s shares. So, for the better part of a decade, the company has poured billions into failed hardware attempts, and no one has been able to stop them. Their latest clunky smart glasses arrived priced at nearly 3x the competition and were discounted as essentially dead on arrival. Through all of this, there has been exactly one voice in the building that mattered. And over the last 5 years, the stock has lost about 90% of its value, while the broad market has essentially doubled.

And here’s the part that bothers me. The core business is actually good. They have half a billion daily users who are overwhelmingly young. Exactly the demo advertisers pay up for. But that asset is being starved to fund a hardware war against rivals whose market caps move up or down more in a day than Snap is worth.

Which brings me back to my old first-meeting rule. The structure itself is a disclosure.

A dual-class charter is really just a company dropping its F-bomb in the first meeting. They are telling investors, in plain language, exactly who they’re dealing with and how much their input will be valued.

But where my first-meeting disclosure was an invitation — here’s who I am now be who you are — and I got back cando. A dual-class charter makes its disclosure with the feedback loop already closed. Here’s who we are, and who you are don’t matter.

So investors respond in the only way left to them. Price.

The market values a daily user on the biggest social platforms in the hundreds of dollars. At Snap, it’s in the teens. Sure, some of that gap may be in the business model. But certainly some of it is in the charter.

Here’s the point for founders to understand. Feedback is not a constraint on your vision. Feedback is insurance on the vision. The feedback loop is there to catch the wrong turn while it's still cheap to correct. Founders who take these multi-class structures public often believe they are protecting their vision from the mob. What they are actually doing is canceling their insurance policy. Alphabet’s judgment held. Snap’s didn’t. And here’s the catch: neither could have truly known in advance which one they’d be.

From the Field: The Sputtering Firework

The other night, celebrating the Fourth of July with family and friends, we let the kids set off fireworks in the cul-de-sac. My son is 11 now, and between the various families out that night, we had kids, parents, and grandparents all represented. A decent crowd of adults was watching over the kids as they were lighting our money on fire. The fireworks themselves were the basic run-of-the-mill kind you can get from Costco, which still feels like an act of rebellion when you’re 11.

Most of the fireworks did exactly what they were supposed to do. The kids would light the fuse, step back and watch it send sparks into the air. When a firework launches cleanly, nobody moves. You know where it’s going, so you know where to stand.

Then one tipped over.

It didn’t spin, explode, or do anything incredibly dramatic. It just kept firing, shot after shot, skidding across the ground and roughly in our direction. And here’s the thing. Nobody panicked and ran inside. What happened was quieter than that. The conversations slowed down. The moms got a little uneasy and started watching much more carefully. The dads took stock of where the exits were and made sure the kids saw what was happening. Not because that firework was more powerful than the others. But because it had no trajectory. A firework going up as designed is a known quantity. A firework on its side could send its next shot anywhere.

The stock market has been doing exactly this since May.

The tape isn’t falling. A decline would at least be a direction. And directions can be managed. This market is trendless. Under the hood, the names that led for a decade have handed off leadership, and the market hasn’t settled on who will carry it going forward. Rallies keep starting and sputtering out. Even blowout earnings have stopped lifting the index. Mandelbrot said markets move in trends, trends break, and in between sits a period of chaos where the past is no guide at all. That stretch is where we are. The firework is on its side, still firing, and everyone is watching very carefully.

The consolation is having a plan before the chaos. It was true in the cul-de-sac, too. Before the first fuse was lit, the decisions that mattered had already been made. Where to stand. Where the water bucket was. Where the unlit pile of fireworks would be kept. We didn’t make those calls mid-sputter. Markets are no different. You can’t schedule the moment the tape tips over. But you can assess your risks, your game plan, and your exits. These can all be known long before you enter a trade. Investors who did that work before they got in aren’t scrambling. They’re just watching carefully, because they know they’re already standing in the right place.

Signal vs. Noise

Quiet Isn’t Calm — When communication shrinks to a smaller surface area, the reaction to it often grows. The less often you speak, the more every word has to carry, and the harder your audience has to adjust when it lands. Silence doesn’t lower the stakes. It concentrates them.

Leverage on Judgment — Removing the voices that can correct your path doesn’t make you right more often. It just makes being wrong that much more expensive. Feedback is not a constraint on vision. It’s the insurance protecting it.

The Tipped Firework — A falling market has a direction, and direction can be managed. A trendless one can put the next shot anywhere. That’s when your plan matters most, and by then it’s too late to make one. Know the risks and your exits before you go in.

One Last Thing

You don't manage a sputtering market by predicting where the next shot lands. Nobody's that good, and the ones who claim to be are selling you something. You do what a cul-de-sac full of adults did on the Fourth. Pay closer attention. Know where the exits are. And make sure the people you're responsible for see what's happening, instead of shielding them from it.

If this letter resonated, I’d love to hear from you. And if you know someone who’d find it interesting, feel free to pass it along.

Until next month,

— Zachary